Well now, it seems private credit is strutting about like a peacock – and not the kind you’d want to invite to dinner. Defaults are climbing higher than a cat on a hot tin roof, reaching levels that would make even the ghosts of 2008 blush while liquidity concerns lurk in the shadows, plotting their next move.

Default Rates Take a Leap in Private Credit Market, Now a Whopping $1.8 Trillion

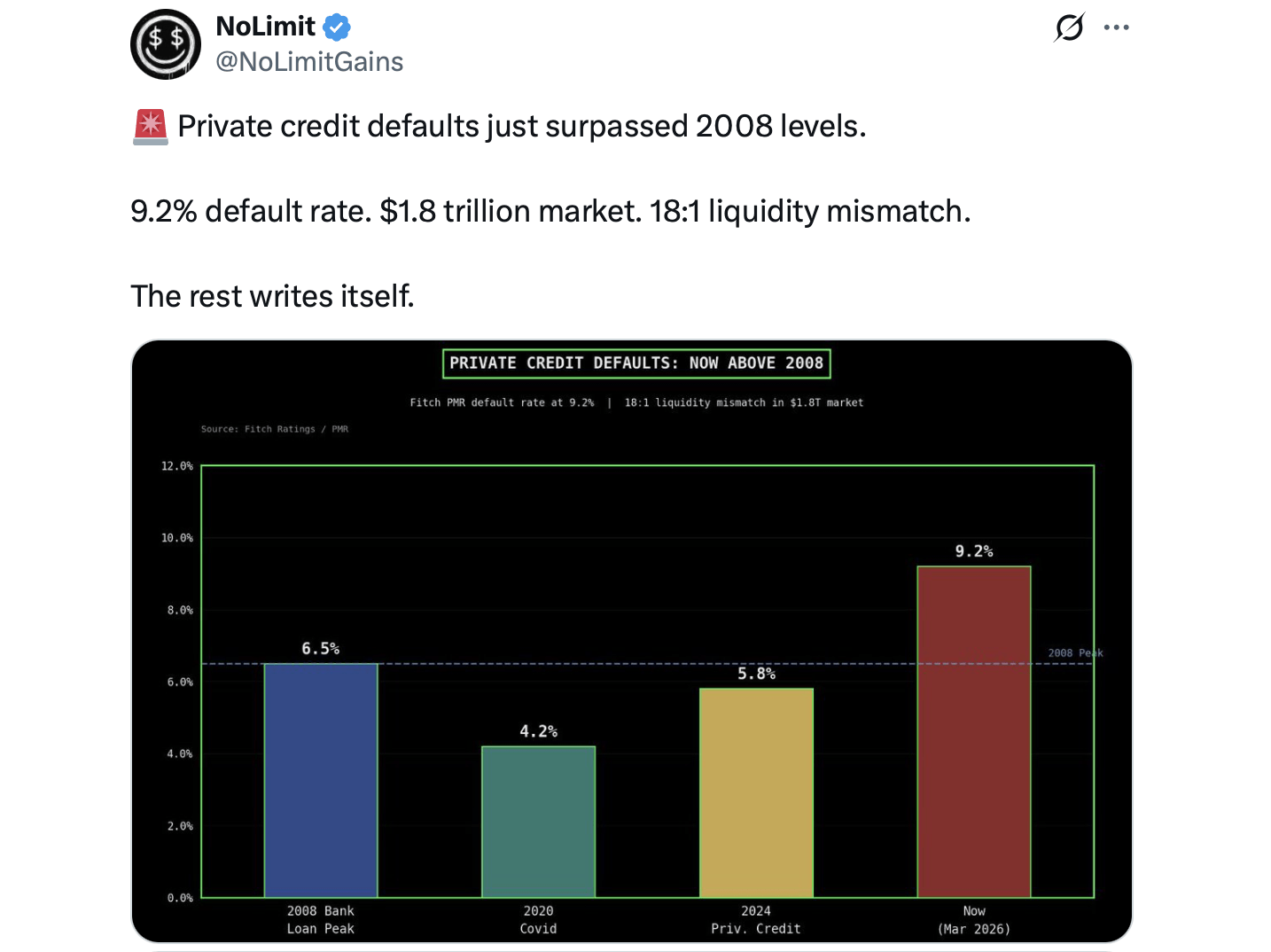

Fitch Ratings has taken off its glasses and reported, bless their hearts, that their Privately Monitored Ratings (PMR) default rate has hit a staggering 9.2% for the full year of 2025. That’s a jump from 8.1% last year and exceeds the famous peaks seen during the financial crisis, which were about as welcome as a skunk at a garden party.

This figure has been bouncing around the financial world like a ping-pong ball, amplified by viral charts and market commentary that point to the ballooning size of the private credit sector – now estimated at a jaw-dropping $1.8 trillion in assets under management. I reckon that’s enough to make anyone’s eyes water.

Private credit, often dressed up fancy as direct lending, involves nonbank institutions handing out loans like candy to middle-market companies. These borrowers usually have an EBITDA less than $100 million and are relying on financing for all sorts of things like buyouts, refinancing, or expansion – a territory banks have mostly vacated faster than a rabbit from a hound.

This retreat opened wide the gates for asset managers like Blackstone, Apollo, Ares, and KKR to build their lending empires. What began as a workaround has blossomed into one of the fastest-growing corners of modern finance, much like a weed in an untended garden.

But let me tell you, growth comes with strings attached.

According to Fitch’s data, defaults are like a bad case of measles, concentrated among smaller borrowers, with firms generating $25 million or less in EBITDA facing a staggering 15.8% default rate, while larger issuers sit pretty at just 4%. The villain here? Higher interest rates have turned floating-rate debt into a costly affair, squeezing those poor companies like a lemon in the summer sun.

However, don’t go throwing your hands up just yet – the headline number comes with a silver lining. Losses remain relatively contained, thank goodness. In many cases, lenders have opted for flexibility over force. Instead of tossing companies into bankruptcy like yesterday’s trash, private credit managers often extend maturities, allow payment-in-kind (PIK) interest, or tinker with the terms. Fitch found that most resolved cases in 2025 delivered near-par recoveries, with only modest losses in a minority of situations.

That distinction is worth noting. Sure, defaults are on the rise, but they aren’t wreaking havoc like the chaotic years of yore. Yet, another issue looms larger than life: liquidity.

The very same market that has swelled to $1.8 trillion operates with a secondary trading capacity so limited it could fit in a teacup – estimated around $100 billion – creating a mismatch between assets and liquidity of about 18-to-1. In simple folks’ terms, that means investors can’t easily exit positions if sentiment turns colder than a witch’s tit in winter.

This tension is already bubbling to the surface. Several large private credit funds are feeling the heat in early 2026, forcing some managers to curtail withdrawals or inject capital to keep things afloat. Publicly traded business development companies (BDCs), which provide a glimpse into the sector, have also been trading at notable discounts to their underlying asset values, much like a yard sale gone wrong.

As noted by Bloomberg, in a recent podcast, Lotfi Karoui from Pimco put it succinctly:

“The big lesson of all of this is that, from an investor standpoint, this is a little bit of a wake-up moment.”

This mismatch becomes especially relevant as private credit expands beyond institutional portfolios into wealth channels. Semi-liquid funds – often marketed with promises of periodic redemptions – may sound like a sweet deal, but the underlying loans remain as stubbornly illiquid as a mule on a hot day.

For now, the system is holding steady. There ain’t no immediate sign of the kind of systemic stress that made 2008 feel like a trip to the dentist, and banks are less directly exposed to this segment. Meanwhile, a growing heap of distressed debt capital is lurking on the sidelines, ready to scoop up troubled assets if conditions take a nosedive.

Looking ahead, the key variables are as familiar as an old boot: interest rates, economic growth, and refinancing conditions. A prolonged period of elevated borrowing costs could nudge more companies toward restructuring, particularly as debt maturities stack up in 2026 and 2027 like dirty dishes in the sink.

Yet, industry forecasts remain as optimistic as a rooster in the morning. Some projections suggest private credit could double again by the end of the decade, driven by the unquenchable demand for yield and flexible financing. If that ain’t the American dream, I don’t know what is.

But mind you, that optimism now comes with a sharper edge, like a double-edged sword. Defaults are climbing, liquidity is finite, and the illusion of easy exits is being tested in real-time – a sobering reminder that even the most sophisticated corners of finance still answer to the cold, hard arithmetic of basic math.

FAQ 🔎

- What is private credit?

Private credit refers to loans made by nonbank lenders to companies, often dancing on the fringes of traditional public debt markets. - Why are defaults rising in private credit?

Higher interest rates have cranked up borrowing costs, putting the squeeze on smaller companies with floating-rate debt. - Are investors losing money from these defaults?

Losses have been kept to a minimum so far due to loan restructurings and high recovery rates – a silver lining, indeed. - What is the liquidity mismatch in private credit?

It refers to the yawning gap between hefty asset holdings and the relatively tiny secondary market capacity for offloading those loans.

Read More

- PayPal’s PYUSD: World Domination or Just Another Coin Flip?

- ETH PREDICTION. ETH cryptocurrency

- OP PREDICTION. OP cryptocurrency

- 🚀 XRP’s Rocket Ride: From Wallets to Your Stock Portfolio! 🚀

- USD PKR PREDICTION

- USD DKK PREDICTION

- STETH GBP PREDICTION. STETH cryptocurrency

- RENDER PREDICTION. RENDER cryptocurrency

- Bitcoin’s Wild Ride: Why Experts Say It’s Stronger Than Ever 😱

- Bitcoin’s Grand Finale: Gold & Silver Eat Dust 🐒🔥

2026-03-19 20:58